Fintech app development is the process of designing, building, and maintaining secure mobile or web applications for financial services — from digital banking and payments to lending, investing, and insurance. The defining difference from ordinary app projects is that fintech app development must satisfy strict regulatory and security requirements (PCI DSS, KYC/AML, PSD2, GDPR) before a single feature ships. For most companies a production-ready MVP takes roughly 4–7 months and a clear tech stack decision made on day one.

At Dreambit we have spent 14 years shipping 150+ products with 5M+ downloads, and fintech is one of our core industries. Below is the practical playbook we use with clients — what it costs, which regulations actually apply, the architecture that keeps auditors happy, and the mistakes that quietly burn budgets.

What is fintech app development?

Fintech app development covers any software that moves, stores, or analyses money or financial data. In practice it splits into a handful of product categories, each with its own compliance and UX expectations:

- Digital banking & neobanks — accounts, cards, transfers, statements.

- Payments & wallets — P2P transfers, QR payments, merchant checkout.

- Lending & BNPL — credit scoring, loan origination, repayment flows.

- WealthTech & investing — brokerage, robo-advisors, crypto.

- InsurTech — quotes, claims, policy management.

- Personal finance & budgeting — account aggregation, analytics, alerts.

The category you choose determines your regulatory load, your integrations, and your timeline far more than your feature wishlist does.

How much does fintech app development cost in 2026?

A realistic range for a custom fintech app in 2026 is $60,000–$250,000+, depending on scope, compliance, and integrations. A lean, single-platform MVP with one core flow and one payment integration usually lands at the lower end; a multi-platform product with lending logic, KYC, and bank integrations sits at the top.

A fintech MVP with secure authentication, one payment provider, KYC onboarding, and a single core flow typically costs $60,000–$120,000 and reaches the app stores in 4–7 months — compliance work alone accounts for 15–25% of that budget (Dreambit project benchmarks, 2026).

The main cost drivers are predictable:

- Compliance & security — audits, penetration testing, encryption, secure infrastructure.

- Third-party integrations — payment gateways, banking APIs, KYC/AML providers each carry setup and per-transaction fees.

- Platform choice — cross-platform (Flutter, React Native) versus two native codebases.

- Team seniority — fintech rewards experienced engineers who have shipped regulated products before.

For a deeper breakdown of what drives software budgets, see our guide on the cost of custom software development in 2026.

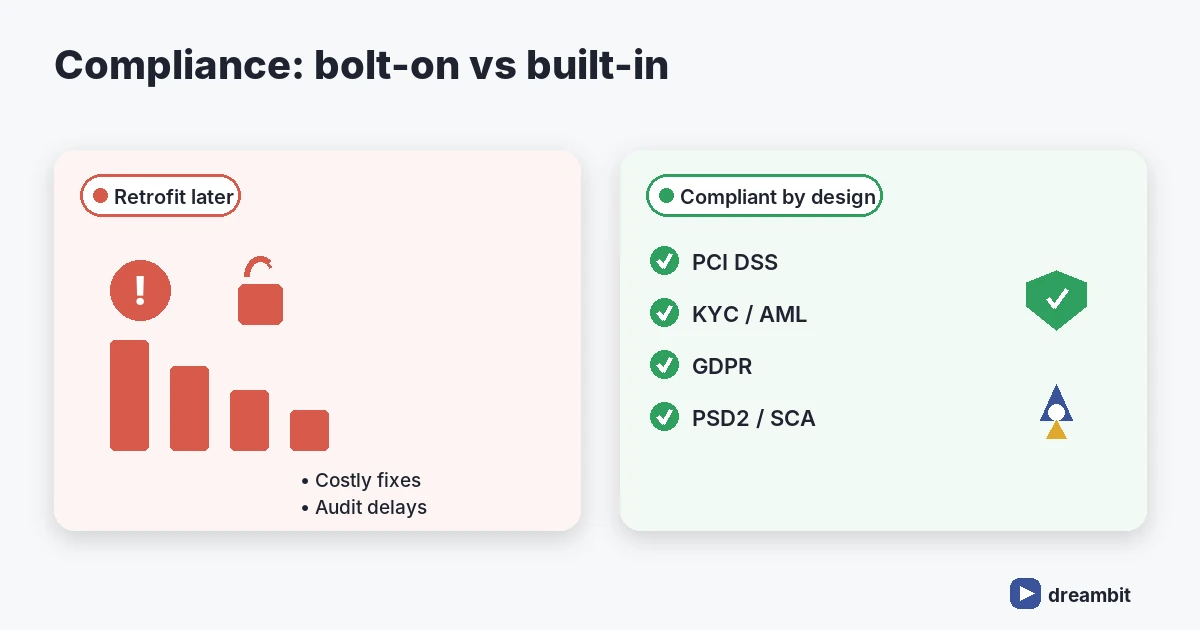

Which regulations and compliance standards apply?

Compliance is not a feature you add later — it shapes your data model, your hosting, and your onboarding. The standards that most often apply to fintech app development are:

- PCI DSS — mandatory if you store, process, or transmit card data. Using a tokenised gateway dramatically reduces your scope.

- KYC / AML — identity verification and anti-money-laundering checks, usually delivered through a specialist provider.

- PSD2 / Open Banking — strong customer authentication (SCA) and secure account access in the UK and EU.

- GDPR / CCPA — data privacy, consent, and the right to erasure.

- SOC 2 — increasingly expected by enterprise partners and investors.

The practical rule we give every client: decide which regulations apply before design starts, because retrofitting compliance is the single most expensive way to build a fintech product.

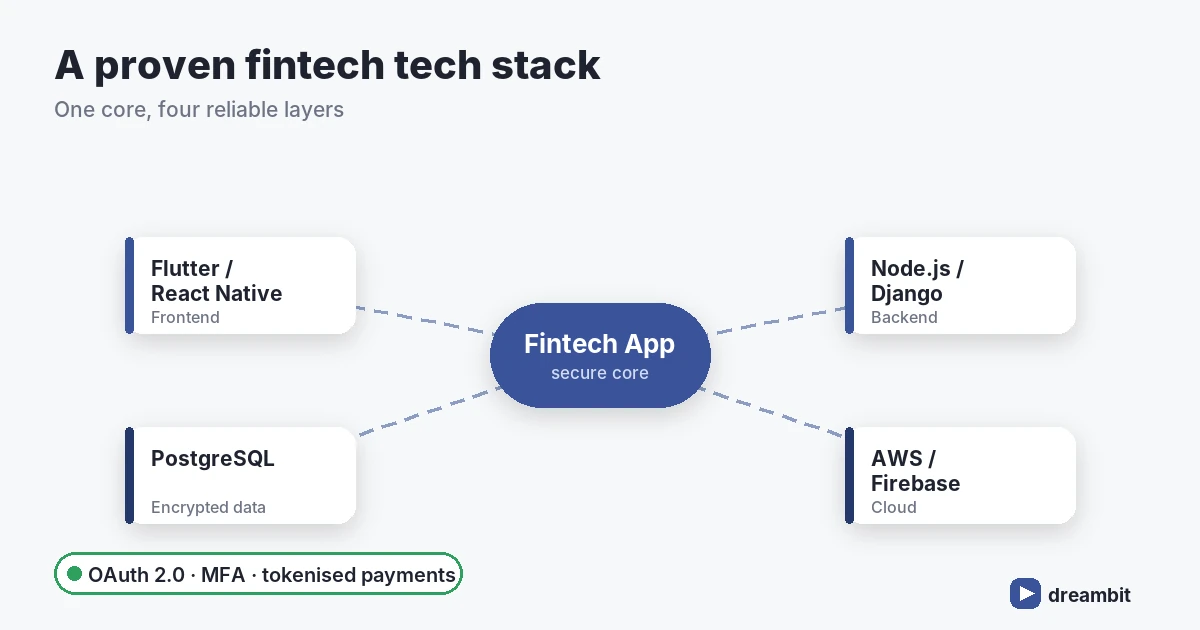

The right tech stack for a fintech app

There is no universally “best” stack, but there is a sensible default for most products. After 60+ MVPs we lean toward a cross-platform front end paired with a strongly-typed, well-audited back end.

Front end

Flutter and React Native let you ship iOS and Android from one codebase, cutting build cost by roughly 30–40% versus two native apps while keeping near-native performance. For finance UIs with heavy animations and consistent branding across platforms, Flutter is our usual recommendation — see why we use Flutter and Firebase for SaaS MVPs.

Back end & infrastructure

- Languages: Node.js (Express/Koa) or Python (Django) for rapid, maintainable services.

- Data: PostgreSQL for transactional integrity; encrypted at rest and in transit.

- Cloud: AWS or Firebase with region controls for data residency.

- Auth: OAuth 2.0, biometric login, and multi-factor authentication by default.

Must-have features for a fintech app

Whatever the category, a credible fintech app ships with a non-negotiable core:

- Secure onboarding with KYC and biometric/MFA login

- Real-time transactions and push notifications

- Encrypted data storage and tokenised payments

- Clear transaction history and exportable statements

- In-app support and fraud-alert flows

- Accessibility and a friction-light UX (finance users abandon fast)

AI is now part of that baseline too — fraud detection, spending insights, and churn prediction. We covered the retention side of this in how we predict user churn and bring users back.

Our fintech app development process

We run regulated builds in five stages, with compliance and security threaded through every one:

- Discovery (1–2 weeks) — scope, regulations, and architecture decisions.

- UX/UI design (2–4 weeks) — flows, prototypes, and accessibility.

- Development (8–16 weeks) — iterative sprints with security reviews.

- QA & security testing (ongoing) — including penetration testing before launch.

- Launch & maintenance — monitoring, updates, and compliance upkeep.

Curious what the opening weeks look like in detail? Here is what we actually do in the first two weeks of a project.

Common fintech app development mistakes to avoid

- Treating compliance as a phase. It is an architecture constraint — bake it in from discovery.

- Storing card data you do not need to. Tokenise through a gateway and shrink your PCI scope.

- Over-building the MVP. Ship one core flow brilliantly before adding modules.

- Ignoring onboarding friction. Every extra KYC step costs conversions; sequence requests carefully.

- Skipping penetration testing. In finance, a single breach can end the product.

Key Takeaways

- Custom fintech app development in 2026 typically costs $60,000–$250,000+, with compliance taking 15–25% of the budget.

- Decide on PCI DSS, KYC/AML, PSD2, and GDPR scope before design begins.

- A cross-platform stack (Flutter/React Native + Node/Python + PostgreSQL on AWS) suits most products.

- Security — encryption, MFA, tokenisation, penetration testing — is the baseline, not a bonus.

- Ship a focused MVP in 4–7 months, then expand based on real usage.

Frequently Asked Questions

How long does fintech app development take?

A focused fintech MVP usually takes 4–7 months from discovery to app-store launch. The variable is compliance: products needing full KYC/AML, lending logic, or bank integrations sit at the longer end, while a single-flow payments or budgeting app can launch faster.

How much does it cost to build a fintech app?

Most custom fintech apps cost between $60,000 and $250,000+ in 2026. A lean single-platform MVP starts around $60,000–$120,000, while multi-platform products with lending, KYC, and banking integrations run higher. Compliance and security typically account for 15–25% of the total.

What compliance is required for a fintech app?

It depends on what you handle. PCI DSS applies if you touch card data, KYC/AML if you onboard users for financial services, PSD2/Open Banking in the UK and EU, and GDPR/CCPA for personal data. Define the applicable standards before design — retrofitting compliance is far more expensive.

Which is better for fintech apps, Flutter or React Native?

Both are solid cross-platform choices that cut build cost versus native. We usually recommend Flutter for finance apps because of its consistent UI across platforms and strong performance with rich, animated interfaces. React Native is an excellent fit when a team already has deep JavaScript expertise.

Is it safe to build a fintech app with a development agency?

Yes, provided the agency has shipped regulated products and treats security as a first-class concern. Look for experience with PCI DSS and KYC, a documented security testing process, and verifiable client results. Dreambit has delivered 150+ apps with a 4.9★ average rating across 114 client reviews.

Build your fintech app with Dreambit

Fintech app development rewards teams that understand regulation, security, and user trust in equal measure. With 14 years of delivery experience, 150+ launched products, and an AI-first approach, Dreambit helps founders and CTOs ship secure financial products that pass audits and win users. Book a free consultation and let us scope your fintech app together.